FCA to continue investigation into motor finance sector

The Financial Conduct Authority has said that it will continue investigations into the “risk of harm” posed by motor finance, with its final findings expected to be delivered in September.

In its FCA motor finance investigation update, published today, the FCA revealed that it had already concluded that “the largest lenders’ approach to credit risk and asset values appears robust” and that “consumers in the lowest credit score range account for a relatively small share of motor finance lending”.

But a rise in payment arrears and concerns surrounding the car retailers’ commission arrangements with lenders has prompted further scrutiny of the sector.

The FCA noted in its report that finance agreements for new and used cars had grown from around 1.2m in 2008 to around 2.3m in 2017, with new finance contracts accounted for 88% of private new car registrations in 2017, up from 59% in 2008.

Personal contract purchase (PCP) agreements have become particularly widespread, accounting for around 66% of the value of new and used car finance lending in 2017 (up from around 34% in 2008), it added, stating that the average value of motor finance contracts had risen 9.4% from just under £13,500 in 2013 to just under £15,000 in 2016.

Motor finance affordability

While the Authority said that “the largest FCA solo-regulated lenders are adequately managing the risk of a severe fall in used car prices, such that this would not materially affect their overall financial soundness”, some consumers remained vulnerable to difficulties in making repayments.

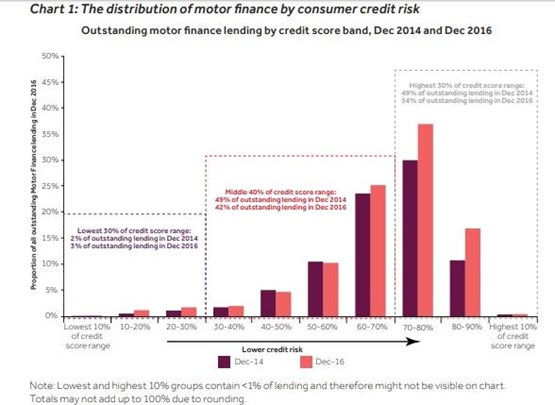

The FCA noted that consumers in the lowest 30% of credit score range accounted for only 2% of outstanding motor finance lending in December 2014 and 3% in December 2016, adding that motor finance lending to consumers in the highest credit score range (lower credit risk) has grown more than lending to consumers in the lowest credit score range (higher credit risk).

Consumers in the highest 30% of credit score range accounted for 54% of outstanding motor finance lending in December 2016, up from 49% in December 2014, it said.

However, 2.4% of accounts in the FCA’s data had one or two missed payments and 0.4% of accounts had between three and five missed payments in the 12 months to December 2016.

By comparison, 1.6% of mortgage accounts were in arrears in Q4 of 2016. For personal loans and credit cards, around 0.3% and 2.2% of customers respectively are two or more payments behind.

The FCA said: “We are mindful that arrears and default rates have increased, in particular for higher credit risk (lower credit score) consumers.

“These rises have been in the context of benign credit and macro-economic conditions. This means that consumer circumstances and their ability to meet repayments could change as a result of changing conditions.”

As a result, the FCA said that it would undertake further work on responsible lending, particularly the approach taken by motor finance lenders to assessment of creditworthiness, including affordability.

Closer scrutiny of commission

In its investigation into car retailers’ commission arrangements with lenders, the FCA analysed agreements between some of the largest lenders (45% of market) and their “top dealers”, between 2013 and 2016.

In its finding the authority noted the various complex arrangements that exist between the two parties and concluded that it would conduct further investigations focussed on relationships where commission structures create a strong link between the dealer commission and the interest rate charged to consumers.

It said: “This can create incentives for dealers to arrange motor finance at higher interest rates. Without adequate systems and controls, this could lead to consumer harm.”

The FCA did acknowledge, however, that the independent dealer segment typically provide a stronger link between dealer commission and the consumer interest rate than in the franchised dealer segment.

Transparency is also set to be put under the spotlight in relation to the information offers to motor finance customers.

The FCA said that, while the terminology and language used in retailers’ finance-related information published online “in general appear to be clear and consistent” it had seen cases where information is “not sufficiently prominent and may not meet our requirements”.

The authority said that continued assessment of this area, which would include mystery shopping exercises, would inform its findings which are set to be published in September.

Industry comments

Commenting on the findings on the first stage of the FCA's review of the motor finance sector, NFDA director Sue Robinson said: "It is positive to see that the Financial Conduct Authority (FCA) has acknowledged that growth in the motor finance sector has been the strongest for lowest risk consumers.

“The FCA has recognised that although motor finance is growing, it is in a sustainable way. We and our members will continue to work closely with the FCA going forward.”

Adrian Dally, Head of Motor Finance at the FLA, echoed Robinson's comments. He said: “We welcome the FCA’s update on its exploratory work in the motor finance market – particularly that most of the growth in the sector has been for those customers with higher credit ratings, that arrears and defaults remain low, and that prudential considerations are being robustly managed.

"It’s also useful that the FCA agrees that motor finance contracts are generally transparent, and provide useful flexibility for customers.”